Catalyst Bins Market Insights

Market Overview

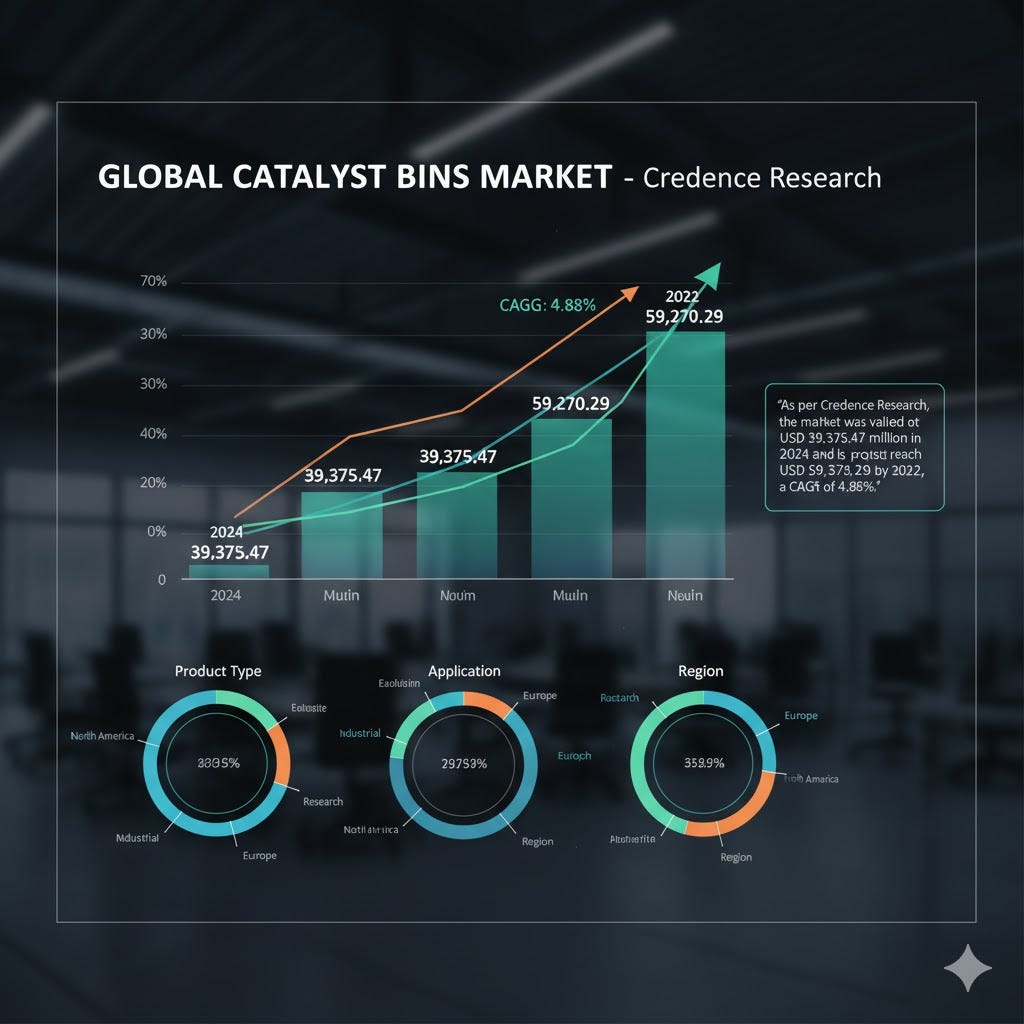

The global Catalyst Bins Market, as per Credence Research, was valued at USD 39,375.47 million in 2024 and is projected to reach USD 59,270.29 million by 2032, at a CAGR of 4.88%. It grows due to rising demand from petrochemical, oil & gas, and chemical industries requiring efficient storage for large-scale catalyst usage. Stainless steel bins dominate due to superior corrosion resistance, durability, and safety compliance. High-capacity bins ranging from 1000kgs to 3000kgs lead the market. Asia Pacific holds 43.9% market share, followed by North America at 28.2% and Europe at 18.9%, driven by rapid industrialization, refinery expansion, and strict regulatory standards.

Source : https://www.credenceresearch.com/report/catalyst-bins-market

Market Drivers

Rising Demand from Petrochemical and Oil & Gas Industries

The Catalyst Bins Market experiences growth due to expanding petrochemical and oil & gas operations globally. It addresses the need for efficient storage and handling of catalysts in cracking, reforming, and polymerization processes. Large-scale refineries prioritize high-capacity, durable bins. It supports operational efficiency and ensures safe transport of sensitive catalysts. Increasing global energy demand and new refinery projects further drive adoption. It benefits from infrastructure development in Asia-Pacific and Middle East regions. Companies focus on offering bins that meet rigorous safety and environmental standards.

Focus on Durable and High-Capacity Designs

The Catalyst Bins Market emphasizes stainless steel bins and other durable materials to meet industrial requirements. It ensures corrosion resistance, long-term reliability, and compliance with strict safety norms. Bins with 1000kgs to 3000kgs capacity dominate due to their balance of storage volume and operational flexibility. It supports industries such as petrochemicals, chemicals, and oil & gas. Manufacturers invest in designs that reduce maintenance costs and enhance performance. It promotes safer handling, reduces environmental waste, and aligns with sustainability initiatives. Growing demand for large-capacity bins drives consistent market expansion.

Market Trends and Opportunities

Increasing Adoption of Stainless Steel Bins

The Catalyst Bins Market shows trends in using advanced, durable materials, which parallels the Catalyst Bins Market adoption of stainless steel. It offers superior corrosion resistance, durability, and safety for industrial applications. Chemical and petrochemical industries prefer it for catalyst handling and storage. It enhances compliance with stringent regulations and minimizes operational risks. Manufacturers continue developing improved designs to increase efficiency and lifespan. It opens opportunities to expand market presence in regions emphasizing industrial safety and sustainability standards.

Expansion into Emerging Markets

The Catalyst Bins Market demonstrates potential in developing regions, mirrored by the Catalyst Bins Market. It benefits from rapid industrialization, refinery expansion, and chemical production growth in Asia-Pacific and the Middle East. Companies establish distribution networks and partnerships to meet rising demand. It addresses increasing energy requirements and industrial modernization initiatives. Adoption of high-capacity, durable bins strengthens market penetration. It creates opportunities for long-term growth and reinforces market stability in emerging economies.

Market Challenges

Stringent Regulatory Compliance and Safety Standards

The Catalyst Bins Market faces challenges in meeting strict safety and environmental regulations. It must comply with local and international standards for handling hazardous catalysts. Variations in regional regulations can delay product deployment. It requires maintaining consistent quality and corrosion resistance to ensure safe storage. Non-compliance can result in operational risks and penalties. It demands continuous monitoring and adherence to evolving industrial guidelines. Addressing these requirements increases operational costs and complexity.

Supply Chain and Handling Constraints

The Catalyst Bins Market must manage logistics for high-capacity, sensitive storage solutions. It faces challenges transporting heavy bins safely across regions. Maintaining integrity and preventing contamination are critical for industrial operations. It requires temperature and handling-controlled processes in some cases. Disruption in supply chains can delay refinery and chemical plant operations. It demands investments in robust infrastructure and advanced logistics. Efficient management ensures timely delivery and reduces operational risk.

Regional Analysis

Asia Pacific: Leads with 43.9% share, driven by rapid industrialization, refinery expansion, and chemical production growth.

North America: Accounts for 28.2%, supported by advanced infrastructure, strict regulatory compliance, and demand for durable bins.

Europe: Holds 18.9%, emphasizing sustainability, environmental standards, and industrial safety.

Latin America, Middle East & Africa: Represent smaller but steadily growing markets due to infrastructure expansion and energy projects.

Key Players

Metso Outotec

Fluor Corporation

UOP Honeywell

Linde plc

Albemarle Corporation

Global Catalyst Systems

Sinopec

Saipem

BASF SE

Baker Hughes

Clariant AG

Go-To Market Strategy

The Catalyst Bins Market should focus on offering durable, high-capacity, and stainless-steel bins for petrochemical, oil & gas, and chemical industries. It leverages strategic partnerships with distributors and industrial clients to expand reach in emerging markets. It emphasizes compliance with safety and environmental regulations to build credibility. It invests in product innovation to improve corrosion resistance, durability, and operational efficiency. It educates end-users on safe handling and long-term benefits. It uses digital platforms and trade exhibitions to enhance visibility. It strengthens brand recognition and ensures consistent supply, supporting industrial growth and market penetration.

Recent Developments

2022: Introduction of high-capacity stainless steel catalyst bins by Metso Outotec.

2023: Expansion of distribution networks in Asia-Pacific and Middle East by UOP Honeywell.

2023: Launch of durable, corrosion-resistant bins by Linde plc for petrochemical applications.

2024: Albemarle Corporation develops high-capacity bins reducing container transfers in refineries.

2024: Regulatory approvals achieved for innovative designs ensuring compliance with safety standards.

Future Outlook

The Catalyst Bins Market will continue to grow with increased demand from petrochemical, oil & gas, and chemical industries. It will adopt larger, more durable bins to improve operational efficiency and safety. It will expand further into emerging markets with rising industrialization. Companies will innovate to enhance corrosion resistance and compliance with strict safety standards. It will address environmental concerns and sustainability initiatives in storage solutions. It will benefit from refinery expansions, energy projects, and chemical production growth. It will remain focused on efficiency, durability, and long-term reliability to meet global industrial requirements.

For full report: https://www.credenceresearch.com/report/catalyst-bins-market