Passive Fire Protection Materials Market Size, Trends & 2032 Forecast

Market Overview

The Fire Protective Materials market encompasses a broad range of products and systems designed to prevent, delay, or contain the spread of fire across buildings, industrial facilities, and critical infrastructure. These materials play a crucial role in maintaining structural integrity during fire incidents while protecting equipment and saving lives. Key product families include thermal insulation materials such as mineral wool and fiberglass, along with advanced intumescent and ablative coatings that provide essential fire resistance for structural steel and other vulnerable components.

Additionally, the market includes fire-resistant boards and panels, firestop sealants, collars, and engineered fire-protection systems used across construction, oil & gas, power generation, manufacturing, and transportation sectors. Increasing global emphasis on building safety, compliance with stringent fire codes, and wider adoption of passive fire protection solutions continue to fuel strong market demand. Innovations such as lightweight intumescent coatings, sustainable low-VOC formulations, and improved installation systems are further accelerating market growth.

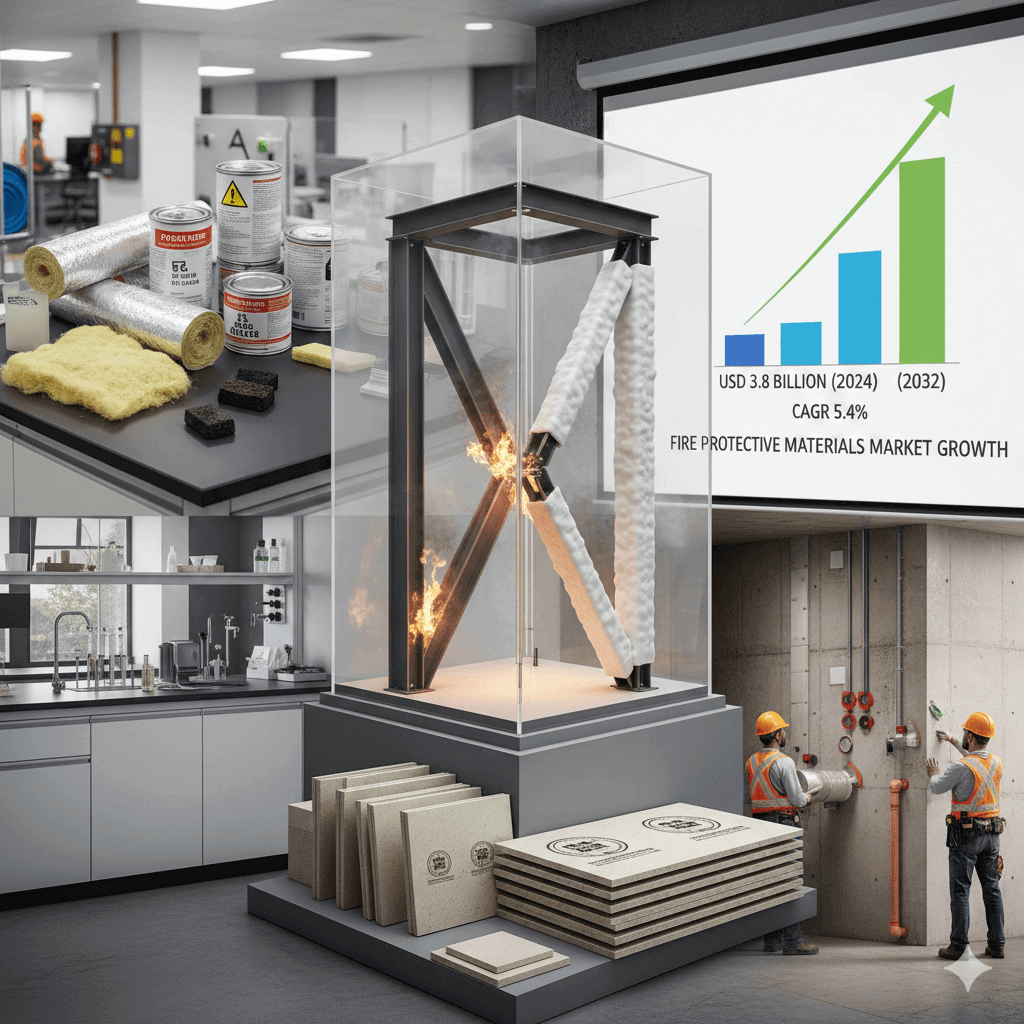

According to Credence Research, the Fire Protective Materials market is valued at USD 3.8 billion and is projected to reach USD 5.8 billion by 2032, registering a steady CAGR of approximately 5.4% during the forecast period. Expansion in infrastructure development, rapid urbanization in emerging economies, and rising renovation and retrofit activities in developed regions are key contributors to this growth. Increasing demand for certified, high-performance fire protection solutions is expected to support continued market expansion across all major geographies.

Source: Fire Protective Materials Market By Size, Share and Forecast 2032

Market Insights

The Fire Protective Materials market is primarily driven by strong demand from the construction sector, which represents the largest end-use segment across both new-build and retrofit projects. Stricter global building codes, enhanced regulatory enforcement, and rising awareness of life-safety standards have compelled builders, architects, and contractors to integrate advanced passive fire protection solutions. Retrofit and refurbishment activities, especially in aging infrastructure across North America and Europe, continue to create consistent market opportunities as older structures are upgraded to comply with modern safety requirements.

Industrial sectors such as oil & gas, power generation, petrochemicals, and manufacturing also contribute significantly to market demand. These industries require high-performance passive fire protection systems capable of withstanding extreme temperatures and safeguarding critical equipment such as vessels, pipelines, and structural steel frameworks. As process safety regulations tighten and the risk of fire-related operational disruptions increases, industrial end-users are prioritizing durable, certified fire protection solutions.

Additionally, the market is experiencing a shift toward advanced materials including intumescent and cementitious coatings, engineered fire insulation products, and modular fireproofing systems. These solutions offer improved aesthetics, faster installation, and reduced maintenance requirements compared to traditional fireproofing materials. Despite strong growth, the market remains highly fragmented, with global multinational corporations competing alongside specialized regional suppliers, each leveraging distinct strengths in formulation expertise, certification capabilities, distribution networks, or local regulatory compliance.

Market Drivers

-

Stricter fire and building codes across global markets

-

Governments are implementing more rigorous fire-safety regulations for commercial, industrial, and multi-residential buildings.

-

Compliance with international fire standards (such as ASTM, EN, and UL) is becoming mandatory in both new-build and renovation projects.

-

Regulatory bodies are increasing audits, inspections, and enforcement efforts, pushing builders to adopt certified passive fire protection products.

-

High-rise construction and complex architectural designs require advanced fireproofing materials to ensure structural stability during fire incidents.

-

-

Rapid urbanization and infrastructure expansion worldwide

-

Emerging economies in Asia Pacific, Middle East, and Africa are experiencing significant growth in construction of commercial buildings, transport networks, and industrial facilities.

-

Mega construction projects—airports, metros, industrial corridors, and smart cities—are fueling demand for high-performance fire protective materials.

-

Increased investment in real estate, public infrastructure, and industrial development continues to strengthen the market’s long-term growth trajectory.

-

-

Accelerating retrofit and refurbishment cycles in developed regions

-

Aging building stock in North America and Europe requires modernization to comply with updated fire-safety standards.

-

Retrofitting old structures often involves installation of firestop systems, insulation upgrades, and intumescent coatings for exposed steel.

-

Government-funded building safety upgrade initiatives, especially for public facilities, commercial complexes, and residential towers, are driving steady demand for fire protective materials.

-

-

Growing safety awareness supported by insurance and risk management demands

-

Insurers and asset owners are emphasizing the need for certified passive fire protection to reduce property loss, business interruption risk, and casualty potential.

-

Fire incidents in high-rise buildings, industrial plants, and warehouses have heightened awareness among developers, facility managers, and regulators.

-

Organizations are increasingly adopting premium fireproofing systems to meet risk assessment requirements and qualify for lower insurance premiums.

-

-

Continuous material innovation and technological advancements

-

Development of lighter, thin-film intumescent coatings provides improved aesthetics, lower application thickness, and better performance under extreme temperatures.

-

High-performance mineral and ceramic-based insulation materials offer enhanced fire resistance and longer protection periods.

-

Innovations in low-VOC, halogen-free, and eco-friendly formulas are gaining traction as sustainability requirements strengthen globally.

-

Prefabricated fire-resistant panels, modular systems, and advanced composites are reducing installation time and improving reliability.

-

Market Trends

Shift Toward Thin-Film Intumescent Coatings

A significant trend in the Fire Protective Materials market is the growing preference for thin-film intumescent coatings, particularly in architectural applications. These coatings provide effective fire resistance while maintaining an attractive aesthetic finish, making them suitable for exposed structural steel in commercial and high-rise buildings. Their reduced coating thickness, ease of application, and improved visual appeal are driving adoption among architects, builders, and contractors who aim to balance safety performance with modern design requirements.

Adoption of Prefabricated and Modular Fire-Protection Systems

The market is also witnessing increasing use of prefabricated and modular fire-protection systems, including pre-coated panels, cladding, and engineered fireproofing modules. These solutions significantly reduce onsite labor requirements, minimize installation time, and ensure consistent performance. As construction timelines shorten and labor costs rise, modular fire-protection systems are becoming a preferred choice for large-scale industrial, commercial, and institutional projects seeking efficiency and reliability.

Growing Focus on Sustainability and Low-VOC Formulations

Sustainability continues to play a central role in material selection, with manufacturers developing low-VOC, halogen-free, and environmentally friendly fire-protection formulations. Regulatory pressure and green building certifications—such as LEED and BREEAM—are accelerating the transition to eco-conscious coatings and binders. This shift is not only reducing environmental impact but also improving indoor air quality, making green fire-protection products increasingly attractive to developers and building owners.

Integration with Digital Building Design Processes

Digitalization in the construction industry is influencing the fire-protection materials market, particularly through the adoption of Building Information Modeling (BIM). Fire-protection components and systems are now being specified earlier in project design cycles, improving accuracy, reducing clashes, and enabling smoother installation processes. Manufacturers offering BIM-compatible design files, digital product libraries, and integrated planning tools are gaining a competitive advantage as digital workflows become standard practice in modern construction.

Rising Demand for Specialized Fire-Protection Solutions

New building materials and energy systems are creating demand for specialized fire-protection solutions. For example, the rising popularity of mass timber construction has led to the development of advanced fire-resistant coatings and panels designed specifically for wood structures. Similarly, the rapid expansion of battery energy storage systems (BESS) in renewable energy infrastructure has increased the need for fire-protection products capable of managing high-energy thermal runaway events. These niche applications represent fast-growing segments within the broader fire-protection market.

Segments

By Product

-

Insulation materials (mineral wool, fiberglass, ceramic fiber)

-

Intumescent coatings (architectural and structural)

-

Cementitious & ablative coatings

-

Fire-resistant boards & panels

-

Firestopping (sealants, collars, wraps)

-

Flame-retardant additives & composites

By Material Type

-

Inorganic (mineral wool, ceramic, cementitious)

-

Organic (intumescent polymers, halogen-free organic systems)

-

Composites / hybrid systems

By End-Use / Application

-

Construction (commercial, residential, institutional)

-

Oil & Gas / Petrochemical

-

Power generation & utilities

-

Transportation (rail, marine, aerospace)

-

Industrial manufacturing

-

Defense & critical infrastructure

By Sales Channel

-

OEM / Original equipment specification

-

Distributors & system integrators

-

Direct to contractors / EPCs

Segments Analysis

Construction (Largest Market Segment)

The construction sector represents the largest share of the Fire Protective Materials market, driven by stringent building codes, the rapid rise of high-rise developments, and significant retrofit activity in aging infrastructure. Demand in this segment is shaped by the need for certified passive fire protection across structural steel, walls, ceilings, service penetrations, and façade systems. Intumescent coatings are widely preferred for architectural applications where structural steel remains visible, offering both fire resistance and aesthetic appeal. Meanwhile, mineral wool insulation continues to dominate bulk fire-insulation requirements due to its cost-effectiveness, thermal stability, and suitability for a variety of construction assemblies. As safety standards advance and urban skylines expand globally, this segment maintains strong momentum.

Oil & Gas and Industrial Facilities

Industrial environments—including oil & gas, petrochemical plants, power generation facilities, and heavy manufacturing—require extremely durable fire-protection systems capable of withstanding intense temperatures, hydrocarbon jet fires, and harsh operating conditions. Cementitious fireproofing materials, ceramic-based insulations, and engineered spray-applied systems are the preferred choices for protecting pipelines, processing units, offshore platforms, structural steel frames, and storage tanks. These segments prioritize long-term durability, corrosion resistance, and compliance with strict process safety regulations. As industrial modernization increases and risk-management standards become more rigorous, demand for high-performance passive fire protection remains strong.

Transportation (Aviation, Marine, and Rail)

The transportation segment relies heavily on lightweight, certified fire-resistant panels, insulation materials, and flame-retardant composites. This market is governed by some of the strictest safety standards, including FAA aircraft regulations, marine SOLAS fire-safety rules, and rail authority specifications. Materials used in aircraft interiors, ship cabins, rail coaches, and cargo compartments must withstand rigorous fire-performance testing while minimizing weight and maximizing energy efficiency. As global passenger mobility increases and fleets are upgraded or expanded, the demand for advanced, lightweight fire-protection materials continues to rise.

Material Shifts in Developed Markets

Across North America, Europe, and other mature regions, there is a clear transition toward thinner intumescent coating systems and non-halogenated flame-retardant materials. This shift is driven by sustainability goals, stricter emissions regulations, and the desire for improved aesthetics and application efficiency. Older, heavier fireproofing systems—such as thick cementitious layers or halogen-based retardants—are increasingly being replaced by modern formulations that deliver equivalent or superior fire performance with reduced thickness, lower toxicity, and better environmental compatibility. These material innovations are reshaping procurement preferences and accelerating the adoption of next-generation fire-protection solutions.

Regional Analysis

North America

North America remains one of the most regulated markets for fire protection materials, driven by strict building codes, insurance requirements, and a mature construction ecosystem. The U.S. continues to see strong adoption of intumescent coatings for commercial and industrial buildings, especially in urban centers with high-rise development. Retrofit demand is accelerating as older structures undergo upgrades to meet modern fire-safety standards. The oil & gas sector, particularly in the Gulf region, also contributes significantly through continuous maintenance and high-specification fireproofing needs.

Europe

Europe leads in sustainability-driven fire protection innovation, with stringent environmental standards and an early shift toward low-VOC, halogen-free, and eco-certified formulations. Countries such as Germany, the U.K., and France invest heavily in passive fire protection for commercial, residential, and industrial infrastructure. Adoption of thin-film intumescent coatings is high due to architectural preferences and strict fire-resistance rating requirements. Ongoing modernization of aging building stocks and energy-efficiency-focused renovations further support market expansion.

Asia Pacific

Asia Pacific represents the fastest-growing region, supported by massive construction activity, rapid urbanization, and expanding industrial output. China, India, and Southeast Asia are key contributors, driven by infrastructure development, high-rise commercial construction, and large-scale industrial projects. Fire safety regulations are tightening across many APAC countries, pushing demand for certified and performance-tested fireproofing materials. The region also shows rising adoption of prefabricated and modular fire-protection solutions due to the scale and speed of development.

Middle East & Africa

The Middle East continues to invest in large commercial, petrochemical, and mega-infrastructure projects, demanding high-durability fire protection systems suited for harsh climatic conditions. Oil & gas remains a major driver, particularly in Saudi Arabia, the UAE, and Qatar, where industrial fireproofing requirements are stringent. Africa is an emerging market, with growth tied to expanding urban centers and gradual adoption of stricter building code frameworks. Investments in transport, airports, and industrial zones are expected to accelerate demand gradually.

Latin America

Latin America shows steady but moderate growth, with Brazil and Mexico leading market adoption. Infrastructure modernization, commercial real-estate development, and industrial expansions contribute to increasing use of fire-resistant materials. Regulations vary significantly across countries, but urban centers are gradually enforcing clearer fire-testing standards. Economic fluctuations occasionally impact construction activity; however, long-term demand remains supported by a rising focus on building safety and risk mitigation.

Top 10 Key Players

-

3M (specialty materials, fire barriers & passive protection solutions)

-

Saint-Gobain (insulation products, fire-resistant boards)

-

Owens Corning (insulation materials)

-

Rockwool International (mineral wool insulation)

-

Johns Manville (building insulation & engineered products)

-

Dow Inc. (specialty resins, coatings feedstocks and adhesives)

-

Huntsman Corporation (specialty chemicals, binder systems)

-

BASF SE (flame retardant additives and chemical solutions)

-

Kingspan Group (insulated panels and building envelope products)

-

RPM International (Carboline, Tremco brands) (protective coatings & firestopping products)

Competitive Analysis

Large Diversified Chemical and Materials Companies

Global chemical and materials giants such as BASF, Dow, and Huntsman leverage their scale, extensive R&D capabilities, and broad product portfolios to maintain a strong market presence. These companies compete primarily on formulation performance, regulatory compliance, and the ability to support complex certification requirements. Their large-scale operations allow them to serve diverse end-use sectors, ranging from construction and industrial applications to specialized coatings, positioning them as reliable partners for architects, contractors, and industrial clients.

Building-Material Specialists

Companies like Rockwool, Owens Corning, and Saint-Gobain dominate the bulk insulation and board segments of the market. Their success is supported by extensive distribution networks, long-standing relationships with contractors, and expertise in delivering standardized, high-volume solutions. These players focus on material quality, consistent supply, and customer support, making them preferred choices for large construction projects and retrofit initiatives, particularly in regions with strict fire-protection codes.

Coatings and Firestopping Specialists

Firms such as RPM International, Kingspan, and Sherwin-Williams-type players specialize in fire-protection coatings, sealants, and sprayed systems. Their competitive advantage lies in certified systems, performance-backed solutions, and extensive contractor training programs. By offering end-to-end support, including installation guidance and maintenance recommendations, these companies ensure optimal performance of their fire-protection systems, particularly in industrial and commercial projects where precision and compliance are critical.

Key Differentiation Factors

Market leaders differentiate themselves through multiple factors, including product fire-rating performance, ease of installation, total installed cost, environmental compliance (such as low VOC and halogen-free formulations), technical support, and certified system approvals. Companies that successfully combine high-performance products with reliable installation support and sustainability credentials gain a competitive edge in both mature and emerging markets.

Barriers to Entry

New entrants face significant barriers in the fire-protection materials market. Certification testing for fire ratings is rigorous and costly, requiring specialized laboratory access and extensive compliance documentation. Established contractor networks and trusted distributor relationships give incumbents an advantage in reaching end-users efficiently. Furthermore, liability concerns and insurance expectations create additional challenges for generic or unproven products, making it difficult for new competitors to achieve immediate market penetration without strategic partnerships or niche specialization.

Recent Developments

Regulatory Advancements Driving Adoption

Recent years have seen governments and regulatory agencies worldwide strengthening fire-safety codes and enforcement measures. These changes have encouraged widespread adoption of advanced passive fire-protection solutions in both new constructions and retrofit projects. Particularly in high-rise commercial buildings and industrial facilities, stricter compliance requirements have pushed manufacturers to innovate and deliver certified, high-performance products.

Product Innovation and Material Advancements

Manufacturers are increasingly focusing on thin-film intumescent coatings, modular fireproofing systems, and eco-friendly, low-VOC formulations. These innovations address both functional and aesthetic requirements, allowing for thinner coatings, faster installations, and improved sustainability. Additionally, specialized solutions are being developed for emerging applications such as mass timber construction, battery energy storage systems, and modern industrial processes, broadening the market’s application scope.

Mergers, Acquisitions, and Strategic Partnerships

The market has witnessed consolidation through mergers and acquisitions, as large chemical and materials companies seek to expand their fire-protection portfolios and geographic reach. Strategic partnerships with regional distributors and contractors are also becoming more common, allowing global players to enhance local market access and compliance support. These collaborations strengthen technical expertise and accelerate adoption of advanced fire-protective solutions.

Digital Integration in Construction

Integration with digital building design tools, particularly Building Information Modeling (BIM), has become a key trend. Fire-protection components are increasingly specified during the design phase, ensuring accurate material planning and installation. Companies offering BIM-compatible product libraries and digital design support are gaining a competitive advantage by improving project efficiency and minimizing installation errors.

Future Outlook (2024–2032)

Steady Market Growth

The Fire Protective Materials market is expected to sustain a steady growth trajectory over the forecast period, with the market size projected to increase from USD 3.8 billion in 2024 to USD 5.8 billion by 2032, reflecting a CAGR of approximately 5.4%. Growth will be driven by continued construction activity, both in emerging urban centers and developed regions requiring retrofits of aging buildings. Regulatory pressures and enhanced safety awareness will remain significant long-term demand drivers.

Emerging Applications and Material Innovations

New applications, including mass timber protection, battery energy storage systems, and advanced industrial processes, will create additional opportunities for specialized fire-protection solutions. Material innovation will continue to reshape the market, with lighter intumescent coatings, low-VOC and halogen-free formulations, and modular prefabricated systems gaining adoption. These advancements will enhance ease of installation, sustainability, and aesthetic appeal, particularly in architectural and high-end commercial projects.

Regional Growth Dynamics

Asia Pacific is expected to remain the fastest-growing region due to rapid urbanization, industrial expansion, and large-scale infrastructure development. North America and Europe will continue to grow steadily, driven by retrofit projects, stringent regulations, and demand for high-performance fire-protection materials. The Middle East and Africa will benefit from large infrastructure and oil & gas projects, while Latin America is expected to see moderate growth as building safety standards gradually evolve.

Opportunities and Challenges

Opportunities exist for manufacturers that can deliver high-performance, sustainable, and certified solutions while supporting contractors and designers through technical guidance and digital integration. However, challenges such as raw material price volatility, regulatory complexities, and liability considerations may affect growth. Companies that strategically combine innovation, compliance, and market reach are likely to gain the largest share of the expanding market.

Conclusion

The Fire Protective Materials market is poised for consistent growth from 2024 to 2032, driven by construction expansion, stringent fire-safety regulations, and growing awareness of building and industrial safety. Innovations in materials, such as thin-film intumescent coatings, low-VOC formulations, and modular systems, are reshaping the competitive landscape and enabling broader adoption across diverse sectors. Emerging applications like mass timber construction and battery energy storage further expand market potential.

Regional dynamics highlight Asia Pacific as the primary growth engine, while mature markets like North America and Europe continue to demand high-value solutions for retrofits and compliance-driven projects. Market leaders that combine product performance, environmental compliance, technical support, and digital integration will be well-positioned to capture significant opportunities. Overall, the market demonstrates a strong outlook with sustainable growth, offering ample opportunities for innovation, investment, and strategic expansion.

Source: Fire Protective Materials Market By Size, Share and Forecast 2032